Home Mortgages Confusing You? Attempt These Tips Out

Created by-Aguirre JarvisHome mortgages can be a bit overwhelming. You do not have to be overwhelmed, though, if you take the time to learn more about them. When it comes to your finances it is best to learn all you can before signing on the dotted line. Keep reading to learn about taking out a home mortgage.

If you are considering quitting your job or accepting employment with a different company, delay the change until after the mortgage process has closed. Your mortgage loan has been approved based on the information originally submitted in your application. Any alteration can force a delay in closing or may even force your lender to overturn the decision to approve your loan.

Do not sign up with the first mortgage lender that you come across. There are so many out there that you would be doing yourself a disservice by being hasty. You should shop around a bit to make sure that the rate you are being offered is fair and competitive.

Start saving all of your paperwork that may be required by the lender. These documents include pay stubs, bank statements, W-2 forms and your income tax returns. Keep these documents together and ready to send at all times. If you don't have your paperwork in order, your mortgage may be delayed.

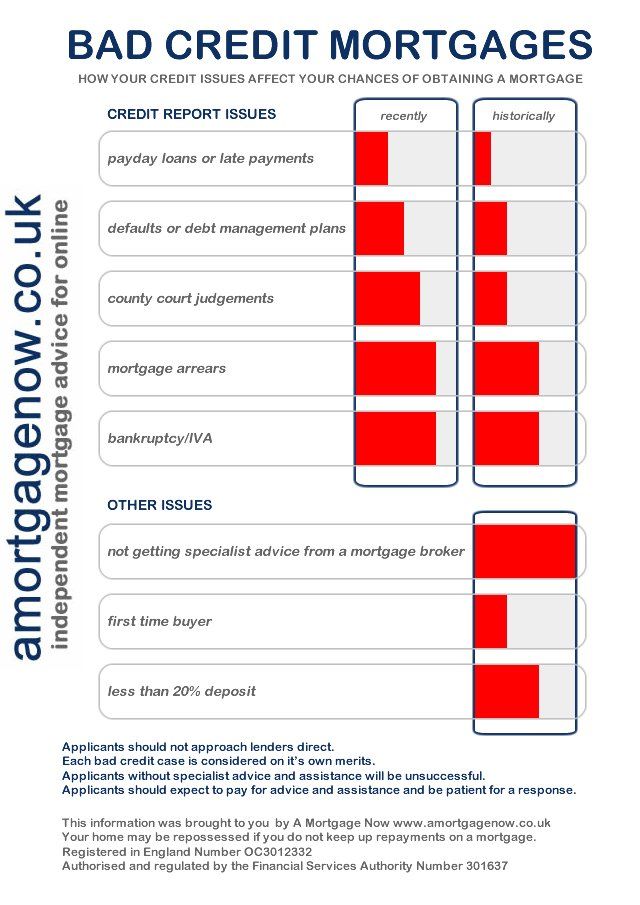

Keep in mind that not all mortgage lending companies have the same rules for approving mortgages and don't be discouraged if you are turned down by the first one you try. Ask for an explanation of why you were denied the mortgage and fix the problem if you can. mouse click the up coming website may also be that you just need to find a different mortgage company.

After you've been approved for your home mortgage and are ready to move in, consider starting a home emergency fund right away. Being a homeowner means always being prepared for the unexpected, so having a stash of cash stored away is a very smart move. You don't want to have to choose between paying your mortgage and fixing a hole in the roof down the road.

Draw up a budget before applying for a home loan. It is important that you know how much you can realistically spend on a mortgage payment. If you aren't paying attention to your finances, it is easy to over-estimate how much you can afford to spend. Write down https://www.gobankingrates.com/banking/banks/best-banks-in-new-hampshire/ and expenses before applying for the mortgage.

Know your mortgage interest rate type. When you are obtaining home financing you should understand how the interest is calculated. Your rate could be fixed or it could be adjustable. With fixed interest rates, your payment will usually not change. Adjustable rates vary depending on the flow of the market and are variable.

Pay at least 20% as a down payment to your home. This will keep you from having to pay PMI (provate mortgage insurance) to your lender. If you pay less than 20%, you very well may be stuck with this additional payment along with your mortgage. It can add hundreds of dollars to your monthly bill.

You likely know you should compare at least three lenders in shopping around. Don't hide this fact from each lender when doing your shopping around. They know you're shopping around. Be forthright in other offers to sweeten the deals any individual lenders give you. Play them against each other to see who really wants your business.

The best way to be sure that you take a mortgage which will continue to be easy to pay off in the future is to take less than the maximum amount you are offered. If you have some extra money at the end of the month, you can put it away into an emergency fund instead of your mortgage.

Most financial institutions require that the property taxes and insurance payments be escrowed. This means the extra amount is added onto your monthly mortgage payment and the payments are made by the institution when they are due. This is convenient, but you also give up any interest you could have collected on the money during the year.

There is more to consider when it comes to a mortgage than just the interest rate. Many other fees may be tacked on as well. Take points, closing costs and other loan terms into consideration. Get quotes from different lenders and then make your decision.

When trying to figure out how much of a mortgage payment you can afford every month, do not neglect to factor in all the other costs of owning a home. There will be homeowner's insurance to consider, as well as neighborhood association fees. If you have previously rented, you might also be new to covering landscaping and yard care, as well as maintenance costs.

Consider a mortgage broker for financing. They may not be as simple as your local bank, but they usually have a larger range of available loans. Mortgage brokers often work with numerous lenders. This allows them to personalize your loan to you more readily than a bank or other finance provider.

Don't feel relaxed when your mortgage receives initial approval. Don't allow yourself to make any changes that may negatively affect your credit score prior to the loan closing. Most lenders check credit scores immediately before closing a loan. If you rush out to get a new car or even more credit cards, they could take the loan away from you for good.

Think about accepting a mortgage for a shorter term. The less time it takes you to pay off your home, the less interest you will pay. Of course, you will pay higher monthly payments on a fifteen year mortgage than on a twenty year mortgage, but in the long run you will save many thousands of dollars. Additionally, owning your home outright will give you tremendous peace of mind.

How flexible is the payment schedule being offered to you? With greater flexibility comes the ability to pay off your mortgage more quickly, but it may also include higher interest rates. Consider how much you will spend over the entire life of the mortgage as you compare your options.

Loans are a risk, and when it comes to a mortgage, they're even more so. Finding the right loan is essential. What you've just read will help you get the best deal on a mortgage that you can.